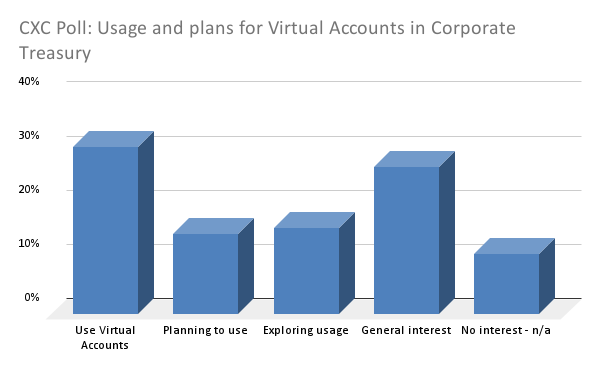

CXC Poll Results - Virtual Accounts

In March 2025, CompleXCountries (CXC) polled members about Virtual Accounts to gauge the current and planned level of usage by corporate treasurers on multinational corporations.

The poll was followed up by a peer discussion and interviews with senior treasury practitioners about their experiences with virtual accounts - the full report will be published in May 2025.

The participants in the poll were 80 senior treasury practitioners from multinational corporations based in Europe, the Americas and Asia.

Users of virtual accounts were also asked about their level of satisfaction, with 80% saying they ‘work as expected’, 16% ‘disappointed’ and 4% ‘exceeded expectations’.These experiences were discussed in a in depth peer discussion [Commentary here - Report (15 pages) available to subscribers]

Some respondents volunteered additional comments which are listed below:

Use - exceed expectations - 'We use virtual accounts and they have exceeded our expectations'

Use - work as expected - use virtual accounts, work as expected (with some banks – not with others)

Use - work as expected & disappointed - Given our experience with virtual accounts, I think we face a mixed picture. The range is somewhere between Exploring / Use - disappointed / Use - work as expected) We have implemented and started using VA in a few countries and for a smaller group of entities, which work as expected and support reconciliation processes and internal allocation of funds, etc. - 3) Unfortunately, in some countries, which we identified as candidates the implementation is still ongoing or did not meet our expectations. This is partly linked to inconsistent requirements / no standards of bank partner.In the implementation process certain critical aspects reg. KYC or regulatory framework became obvious and required additional assessment to be clarified. - 5) In general, we are interested in evaluating and increasing the usage of virtual accounts over time. Therefore we are following the development with interest.

Use - work as expected - Intercompany virtual accounts: we used for ZBA cash pools, FX settlements, IC Netting settlements and other ad hoc IC settlements. It’s also used to avoid opening bank accounts in foreign currency if the entity only has IC trading flows. We are planning to implement COBO/POBO structure and use IC virtual accounts to replace foreign currency bank accounts (with external customers and suppliers). Bank virtual accounts: we use them in China for incoming flows, it helps the automatic reconciliation process.

Use - disappointed implemented virtual bank accounts in 2019, however in 2024 we removed the virtual bank account solution

Planning to use - (CXC member based in India) Banks don’t seem very keen to sell the product or expand usage by clients but planning a deep dive to see if there are truly any benefits

Exploring - The ease of new opening accounts appeals but I am still unsure of tax and regulatory compliance and of cybersecurity risks. They seem to have been around for ages without significant uptake. Currently waiting on the sidelines.

Exploring - We are exploring virtual accounts, subject to OBO structures implementation and systems limitations.

Not interested - Virtual Accounts have limited applicability to our business operations. While they offer value for businesses managing collections from multiple customers by simplifying identification, their utility in payables is minimal. This is primarily because virtual accounts are not equipped to process check payments.

Not interested - no longer interested. We explored VA’s a couple years back after the banks hyped them up as the next big thing. We opened an experimental VA but as we progressed in our discussions with the banks we discovered that VA’s cannot replace existing AR accounts. In order to have an AR VA account it must be a brand new account, new account #, etc and the effort to migrate collections activity to new accounts wasn’t worth it.